Working Capital Cycle Explained: Unlock Your Business Cash Flow Today!

What if the secret to doubling your available cash isn’t selling more products, but simply moving your money faster? According to a 2023 study by U.S. Bank, 82% of small businesses fail because of poor cash flow management. That is a staggering number, but it doesn’t have to be your reality! You know the frustration of watching inventory sit on shelves while payroll deadlines loom like a dark cloud. It’s exhausting to chase slow-paying customers when you have big plans for growth. Look on the Bright Side! We have the working capital cycle explained so you can stop stressing and start scaling.

You’re about to master the mechanics of your cash flow and learn exactly how to shorten your cycle to fuel non-stop business growth. We’ll show you how to turn those “maybe later” payments into “cash in hand” immediately. This guide breaks down the simple math behind your liquidity and provides three actionable steps to get your money moving today. No hidden fees, no complicated jargon; just a clear path to the financial freedom your business deserves. Let’s get started!

Key Takeaways

- Turn your net assets into cold, hard cash faster and uncover the real truth behind your business health today!

- Get the working capital cycle explained in simple terms to master the three pillars that control your cash flow.

- Use our “no-math-degree-required” formula to pinpoint exactly where your money is hiding and how to reclaim it.

- Shorten your cycle to fuel massive growth and secure the hassle-free funds you need to hire, market, and scale!

- Bridge any cash gaps immediately with a high-energy funding boost that keeps your business moving at full speed!

The Pulse of Your Business: The Working Capital Cycle Explained

Your business is a living, breathing thing. To keep it thriving, you need more than just a great product. You need cash flow! The working capital cycle explained in plain English is simply the time it takes to turn your business activities into cold, hard cash. While many owners focus only on profit, the Working Capital Cycle (WCC) is the real truth-teller of your financial health. You can be profitable on paper but still find yourself “cash poor” if your money is locked away in unpaid invoices or dusty inventory. We want to help you unlock that cash today! Mastering this cycle is your first step to hassle-free growth and a brighter future for your company.

To better understand this concept and how it impacts your daily operations, watch this helpful video:

Why Every Day Matters in Your Cash Loop

Time is your most valuable asset. In the high-speed 2026 economy, every second your cash stays trapped is a missed opportunity. A shorter cycle means you slash your reliance on expensive emergency debt immediately. This isn’t just about accounting; it’s about your peace of mind! You deserve the psychological relief of knowing exactly when cash will hit your account. When you optimize this loop, you secure the freedom to pivot and scale without waiting on slow-paying clients. If you need a boost to bridge the gap, you can apply for funding and get a response in as little as 15 minutes. Look on the Bright Side! Your cash should work as hard as you do.

The Difference Between Working Capital and the Cycle

Understanding the working capital cycle explained through the lens of velocity changes how you view your bank account. Let’s clear up the confusion. Working Capital is a simple dollar amount. You calculate it by taking your Current Assets and subtracting your Current Liabilities. It tells you what you have on hand. The cycle is different because it’s a time measurement. It tracks how many days your capital stays in motion before returning to you. The cycle is the velocity of your business liquidity! When your money moves faster, your business grows faster. No credit? No problem! We’re here to help you speed things up so you can focus on what you do best.

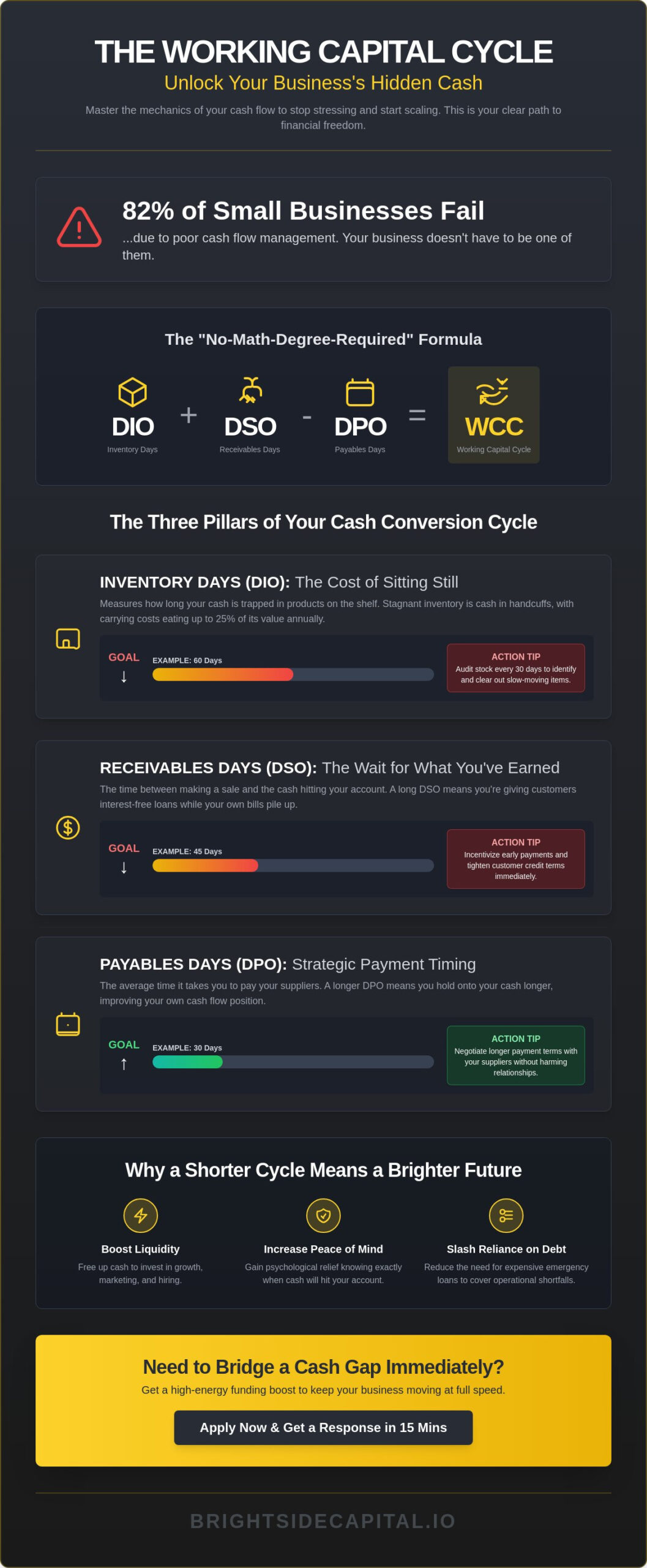

The Three Pillars of the Cash Conversion Cycle

Mastering your cash flow starts with understanding the three forces pulling at your bank account every day. These are Inventory, Receivables, and Payables. Think of them as the gears of your profit machine. When they sync up, your business flies! When they grind, cash gets stuck. This working capital cycle explained simply is a balancing act that you can win. You aren’t at the mercy of the market. You’re in the driver’s seat! Bright Side Capital is here to help you fine-tune these gears so you can focus on growth instead of survival.

Inventory Days (DIO): The Cost of Sitting Still

Receivables Days (DSO): The Wait for What You Earned

Days Sales Outstanding (DSO) is the gap between the moment you make a sale and the moment the cash actually hits your account. Waiting on “net-30” or “net-60” terms can send your stress levels through the roof. If your average DSO is 45 days, you’re essentially providing interest-free loans to your customers while your own bills pile up. You deserve to get paid for your hard work immediately! Shortening this gap is the fastest way to inject liquidity into your operations. Check out our blog for expert tips on managing customer credit and incentivizing early payments. You can master the working capital cycle explained in your own ledger by tightening these terms today.

Payables Days (DPO): Using Time to Your Advantage

Days Payable Outstanding (DPO) tracks how long you take to pay your own suppliers. In the world of cash flow, “slow and steady” is a brilliant move. Stretching your DPO allows you to keep cash in your own account for a longer period. This gives you a larger cushion for unexpected opportunities. The goal is to maximize this window without damaging your reputation. Maintain strong vendor relationships through transparent communication. You can use the working capital cycle formula to find the perfect sweet spot between your DSO and DPO. If you need a temporary bridge while you optimize these pillars, apply for funding today and get the hassle-free cash you need to keep moving forward!

Calculating Your Success: The Working Capital Cycle Formula

Get ready to see your business in a whole new light! Understanding the numbers behind your cash flow is the fastest way to unlock massive growth. Don’t let the math scare you. This is the map to your treasure! The working capital cycle explained simply is just three numbers working together to tell the story of your cash. When you master this formula, you gain total control over your financial future.

Here is your master formula for success: Inventory Days (DIO) + Receivables Days (DSO) – Payables Days (DPO) = Your Working Capital Cycle. It is that simple. This number tells you exactly how many days your cash is tied up in the daily grind before it returns to your pocket as profit.

Step-by-Step Cycle Calculation

Let’s break this down with a no-math-degree-required approach. First, find your Days Inventory Outstanding (DIO). Use this simple calculation: (Average Inventory / Cost of Goods Sold) x 365. This tells you how long your products sit on the shelf before a customer grabs them. Next, find your Days Sales Outstanding (DSO) by using: (Average Accounts Receivable / Total Revenue) x 365. This reveals how fast your customers actually send you money after the sale. Finally, calculate your Days Payable Outstanding (DPO): (Average Accounts Payable / Cost of Goods Sold) x 365. This shows how much time your suppliers give you to pay your bills.

Imagine you run a busy construction firm. If your materials sit for 45 days and your clients take 30 days to pay their invoices, but you pay your lumber yard in 20 days, your cycle is 55 days (45 + 30 – 20). You need to fund 55 days of operations out of your own pocket! Knowing this number allows you to plan for greatness instead of worrying about the next payroll.

Positive vs. Negative Working Capital Cycles

A positive cycle means you are currently waiting for cash. You have already paid for your materials and labor, but the customer’s payment hasn’t hit your bank account yet. Most growing businesses operate this way. According to industry benchmarks for working capital, these cycles vary significantly depending on whether you are in retail, manufacturing, or services. If your cycle is positive, you need a reliable partner to bridge the gap.

The “Holy Grail” of business is the Negative Working Capital Cycle. This happens when you get paid by your customers before you even have to pay your suppliers. It is like getting an interest-free loan every single month! While most businesses fall somewhere in the middle, you can move closer to the “bright side” by speeding up your collections and negotiating better terms with vendors. If your cycle is stretching too long, don’t sweat it. Look on the Bright Side! You can apply for hassle-free funding in just 15 minutes to keep your momentum high while you wait for those big checks to clear. No stress, no waiting, just pure business momentum!

Why a Shorter Cycle Means a Brighter Future

Velocity is the secret sauce of every high-growth business. When your cash moves faster, your business grows faster. It’s that simple! A shorter cycle means you have immediate access to funds for aggressive marketing campaigns, vital equipment upgrades, and hiring the best talent. You stop being a spectator in your industry and start being a leader. Speed is your competitive advantage.

Strategies to Tighten the Loop

Start by incentivizing your customers to pay faster. Offer a 2% discount for payments made within 10 days. This small move drastically shortens your Days Sales Outstanding (DSO) and puts cash in your pocket immediately. On the flip side, talk to your vendors. Negotiating to extend your payment terms from 30 to 45 days keeps your cash working for you longer. To really supercharge your results, consider using Equipment Financing to invest in automated inventory tracking. Better technology means lower inventory days and zero wasted stock!

The Dangers of a Long Working Capital Cycle

A long cycle is a silent profit killer. The biggest risk is “overtrading,” which happens when you grow so fast that you literally run out of cash to fulfill new orders. This is the “Growth Trap.” According to a study by U.S. Bank, 82% of small businesses fail because of poor cash flow management. A long cycle makes you vulnerable to sudden market shifts or a single late paying client. Don’t let your success become your downfall. Proactive planning ensures you have the liquidity to handle any curveball the market throws your way. No stress, no problem!

Ready to see how much cash you can unlock for your business today? We make it easy to get the capital you need to bridge the gap and keep your momentum. Apply for funding now and get a decision in minutes!

Fueling the Cycle: How to Bridge Cash Gaps Immediately

You’ve seen how the working capital cycle explained in the previous sections can sometimes feel like a slow-motion race. You’re doing everything right. You’re selling products and landing big contracts. But then you hit a wall. You’re waiting 60 or 90 days for clients to settle their invoices while your own bills are due tomorrow. This is the “gap” that kills momentum. Sometimes your business doesn’t just need a nudge; it needs a high-energy boost to keep the engine running. Working capital funding acts as a high-speed bridge over those cash flow canyons. It ensures you never have to turn down a new opportunity because your cash is tied up in inventory or accounts receivable.

Look on the Bright Side! You don’t have to stay stuck in a cycle of waiting. We believe in radical accessibility. That means getting you the funds you need in as little as 24 hours with no strings attached. This isn’t about taking on a heavy burden of debt. It’s about unlocking the value already sitting on your balance sheet. When you bridge the gap, you regain control. You can pay your team, stock your shelves, and scale your operations without checking your bank balance every five minutes. It’s fast, it’s reliable, and it’s built for winners who want to move at the speed of light.

When to Use a Working Capital Line of Credit

A startup business line of credit is your most powerful tool for managing early-stage growth. New ventures often face massive gaps between purchasing raw materials and seeing the first dollar of profit. You can use this line of credit to cover seasonal dips or make huge inventory purchases when prices are low. Don’t let a temporary dip in cash stop your long-term vision. The real power lies in the “interest-only” payment structure. You only pay for the funds you actually draw down. If you don’t use it, you don’t pay. This gives you a safety net that costs nothing until you decide to leap. It’s the ultimate “No Stress” solution for the modern entrepreneur.

Get Started with Bright Side Capital

We’ve stripped away the cold, intimidating nature of traditional banking. You won’t find any hidden fees or mountain-high stacks of paperwork here. Our process is built for speed because we know time is money. You’ll get a response in just 15 minutes. That’s faster than a coffee break! Whether you’re in a restricted industry or you’re worried about your credit score, we want to talk. We focus on where your business is going, not where it’s been. This working capital cycle explained today proves that timing is everything. Don’t let another day go by while your growth sits on the sidelines. Apply for funding right now and experience the Bright Side difference. Your cash is out there. Let’s bring it home!

Ignite Your Business Momentum and Scale Faster

You now have the working capital cycle explained so you can master the three pillars of your cash conversion cycle. By tracking your inventory days and optimizing your payables, you’ll stop leaving growth to chance. Recent data from the U.S. Bureau of Labor Statistics shows that roughly 20 percent of small businesses fail within their first year; many of these struggles stem directly from cash flow gaps. Don’t let your business become a statistic when you can bridge any gap immediately. We believe in your vision and provide the fuel to keep you moving forward. You shouldn’t have to wait weeks for a bank’s approval or jump through endless hoops just to access your own potential. We specialize in radical accessibility and lightning-fast speed. Get a response in just 15 minutes and secure your funds in under 24 hours. No credit requirements? No problem! We even provide funding for restricted industries that traditional banks often avoid. It’s time to fuel your next big move with total confidence and zero stress. Ready to bridge your cash gap? Get your hassle-free funding in 24 hours! Look on the Bright Side! Your success is just one click away!

Frequently Asked Questions

What is a good working capital cycle length?

A healthy working capital cycle typically lasts between 30 and 45 days for most small businesses. Retailers often aim for even shorter cycles, while manufacturers might see cycles extending to 90 days. Keep your cycle as short as possible to unlock cash for growth! A shorter cycle means you get paid faster and keep your momentum high. Look on the Bright Side! You can use that extra cash to grab new opportunities immediately.

How does the working capital cycle affect business valuation?

A shorter cycle increases your business valuation because it proves you manage cash efficiently. Investors look for a low “Days Sales Outstanding” ratio, often under 45 days, to determine risk. Efficient cash flow makes your company look like a winner! Use this working capital cycle explained guide to tighten your operations and boost your company’s worth right now. No complicated math; just faster cash and higher value!

Can a business have a negative working capital cycle?

Yes, companies like Amazon or Dell often operate with a negative cycle. This happens when you collect cash from customers before you have to pay your suppliers. It’s a financial superpower! If your accounts payable period is 60 days but you collect cash in 15 days, you have a 45 day negative cycle. This gives you free money to reinvest in your business today!

What is the difference between the working capital cycle and the cash conversion cycle?

There’s no difference; these terms describe the same process of turning resources into cash. Both metrics measure the time from buying inventory to receiving payment from customers. Understanding the working capital cycle explained here helps you track how long your cash is tied up. Use either term to monitor your speed! The goal is always to get that cash back into your bank account as fast as possible.

How do I improve my working capital cycle without losing customers?

Offer a 2% discount for payments made within 10 days to speed up collections. This “2/10 net 30” strategy keeps customers happy while filling your pockets sooner. No pressure; just a win, win! You can also negotiate with suppliers to extend your payment terms to 45 or 60 days. This keeps cash in your business longer without affecting your service quality at all!

Why is my working capital cycle increasing even though sales are up?

Rapid growth often causes “overtrading,” where your inventory and accounts receivable grow faster than your cash reserves. If sales jump 20% but collections slow down, your cycle length will spike. Don’t worry! This is a common growing pain for successful businesses. Secure a quick line of credit to bridge the gap and keep your sales engine running at full speed!

Does a long working capital cycle mean my business is failing?

Not necessarily, but it does mean your cash is trapped. A cycle over 90 days often signals that you need better collection processes or inventory management. High growth can temporarily stretch your cycle. No credit? No problem! You can still find ways to shorten the cycle and get your cash flowing again. Look on the Bright Side! Every business can optimize and win.

How much working capital should I keep on hand?

Aim for a current ratio between 1.2 and 2.0 to ensure you can cover all short term debts. This means having $1.50 in assets for every $1.00 in liabilities. Keeping this buffer ensures you never miss a beat when bills come due. Get that peace of mind today! Having a solid cash cushion allows you to focus on growing your business instead of stressing over daily expenses.